As featured in Room 151

We last published our views on the economic impact of the Middle East war on 9 March. The two weeks since then have been fraught with more casualties on both sides, daily volatility in energy prices and remarkable posts by President Trump on his Truth Social feed.

Last Wednesday, 18 March, saw particularly strong volatility in financial markets. On that day, Israel hit Iran’s northern side of the South Pars Gas Field. A few hours later, Iran retaliated by attacking Qatar’s giant Ras Laffan refinery on the south side of that same gas field. In the evening, Donald Trump threatened to ‘massively blow up the entirety of the South Pars Gas Field’ if Iran attacked the Qatari side again.

Why was last Wednesday particularly important?

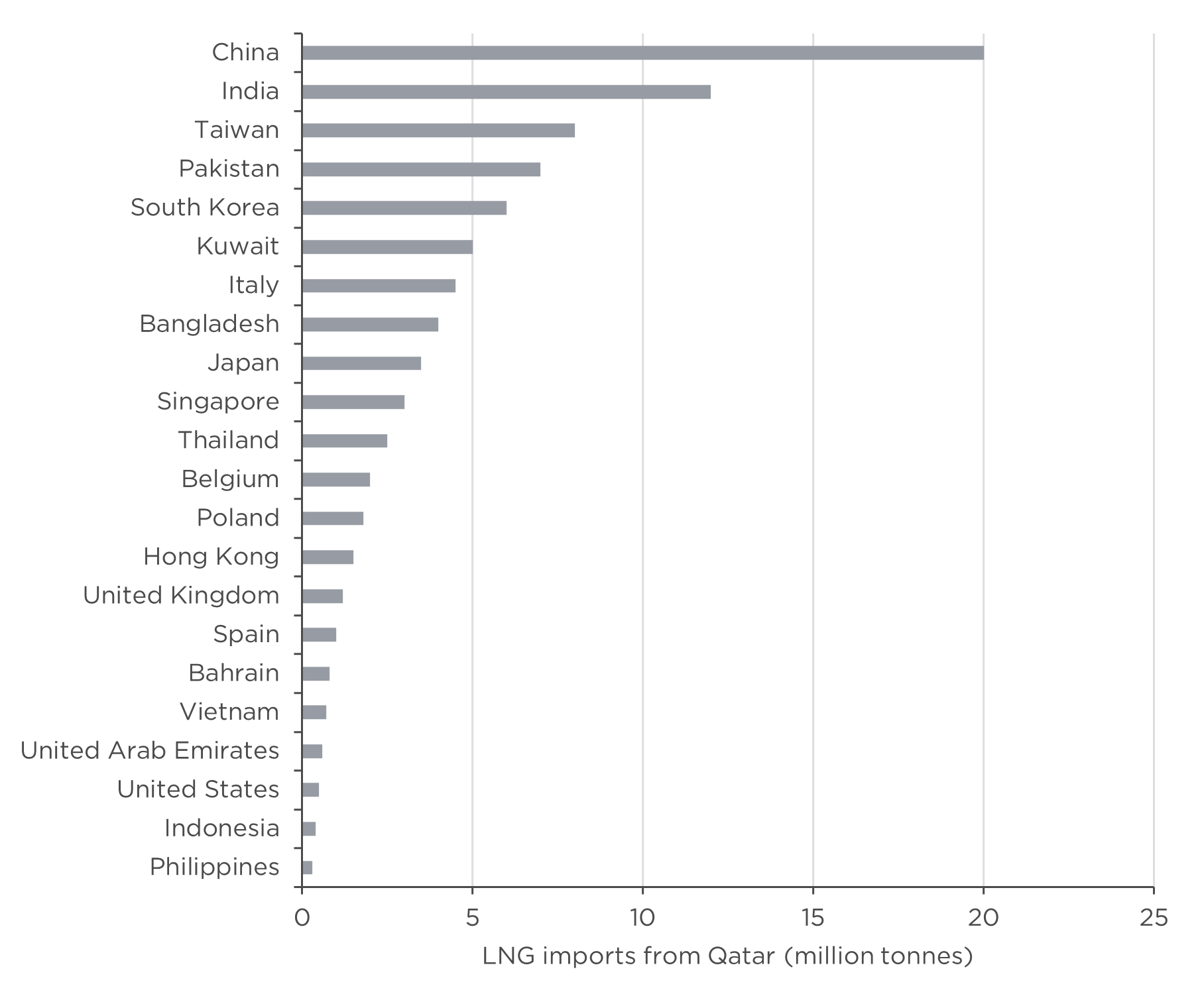

South Pars is the world’s largest natural gas field. It underpins Qatar’s dominance in liquified natural gas (LNG) and represents one-fifth of global supply. Next to producing LNG, the Ras Laffan refinery is responsible for vital by-products such as helium, used in medicine and in semiconductor manufacturing, and ammonia, used as a fertiliser but also in explosives. At Ras Laffan, Qatar loads these products onto ships that supply the world, including economic giants such as China and India.

Figure 1. Most of Qatar’s LNG exports go to Asia

Source: Bloomberg, CCLA estimates

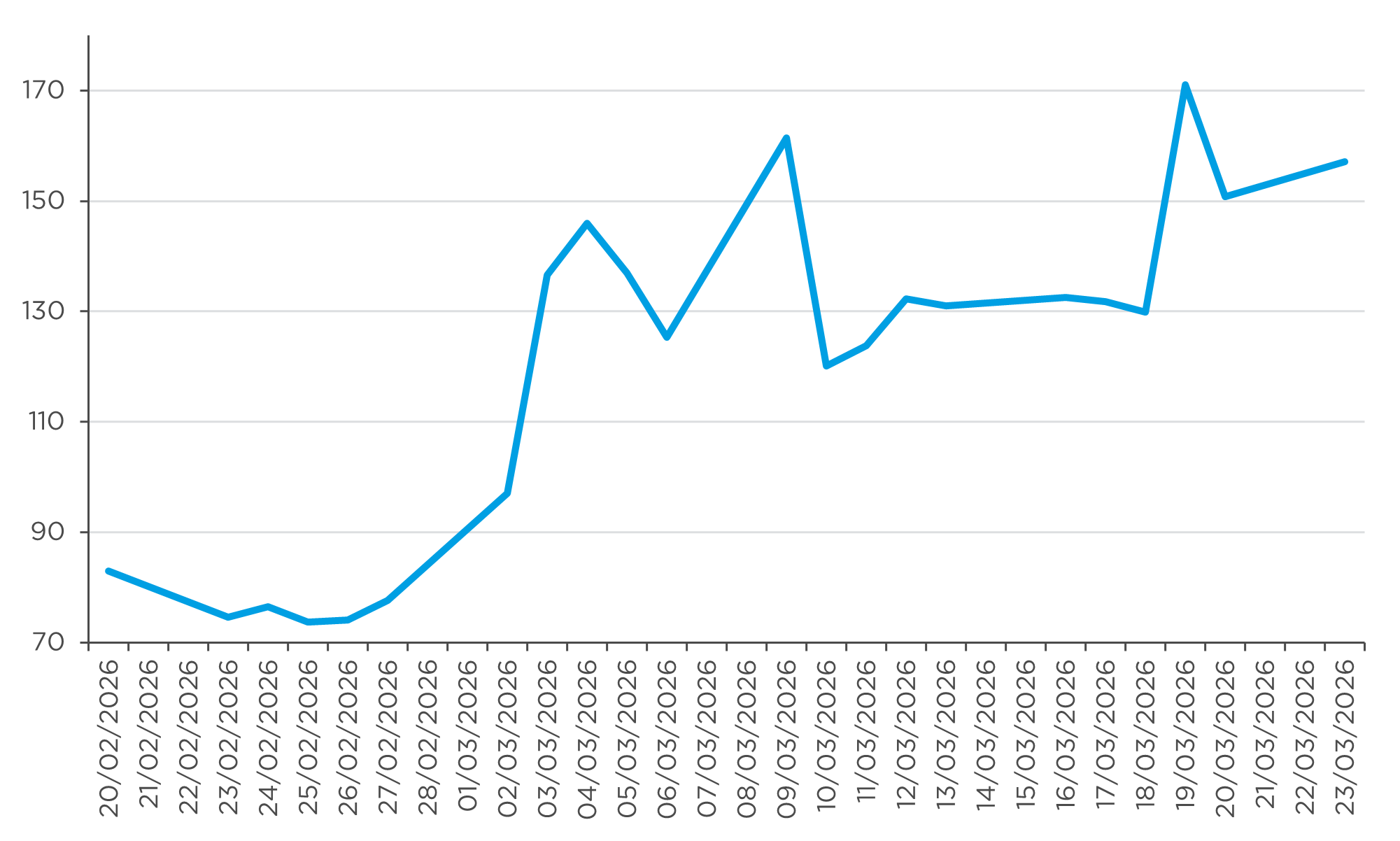

Last Wednesday’s destruction led to a 36% jump in UK natural gas prices by the morning of Thursday 19 March. Thursday’s gas price of 170 pence per therm is the highest during this war so far. It is, however, only a fraction of prices during Russia’s full-scale invasion of Ukraine in 2022, when they reached 640p per therm.

Figure 2. LNG price per therm (pence), February-March 2026

Source: Bloomberg

Energy represents around 6% of the basket that makes up the UK’s consumer prices index (CPI). A 10% increase in energy prices, therefore, could raise CPI inflation by 0.6%. That’s significant on its own, even before more price rises that might follow, as firms might start passing on their increased costs to consumers.

The Bank of England ‘stands ready to act’

Thursday 19 March was also the day on which the Bank of England (BoE) announced its latest policy decision on interest rates. The BoE’s Monetary Policy Committee (MPC) voted unanimously to keep Bank Rate unchanged at 3.75%. After the war broke out, investors had widely come to expect this decision. But the fact that the MPC voted unanimously was a surprise. Investors had expected that some members would continue to prefer a rate cut.

The MPC’s meeting minutes state that the BoE ‘stands ready to act as necessary to ensure that CPI inflation remains on track to meet the 2% target in the medium term’. They also outline that the BoE has raised its expectation for inflation in the second quarter of 2026, from 2.1% p.a. to between 3% and 3.5%. Pertinently, several policymakers indicated that they would consider raising interest rates to stop inflation from getting ingrained in the UK economy.

The sharp rise in energy prices, combined with an MPC that might raise interest rates, sent market interest rates higher. That made Thursday’s rise one of the most substantial corrections in my 14 years as a money market portfolio manager. Before the war, investors broadly expected one or two cuts in the BoE’s Bank Rate before the summer. Now, they expect at least two increases over that same time horizon.

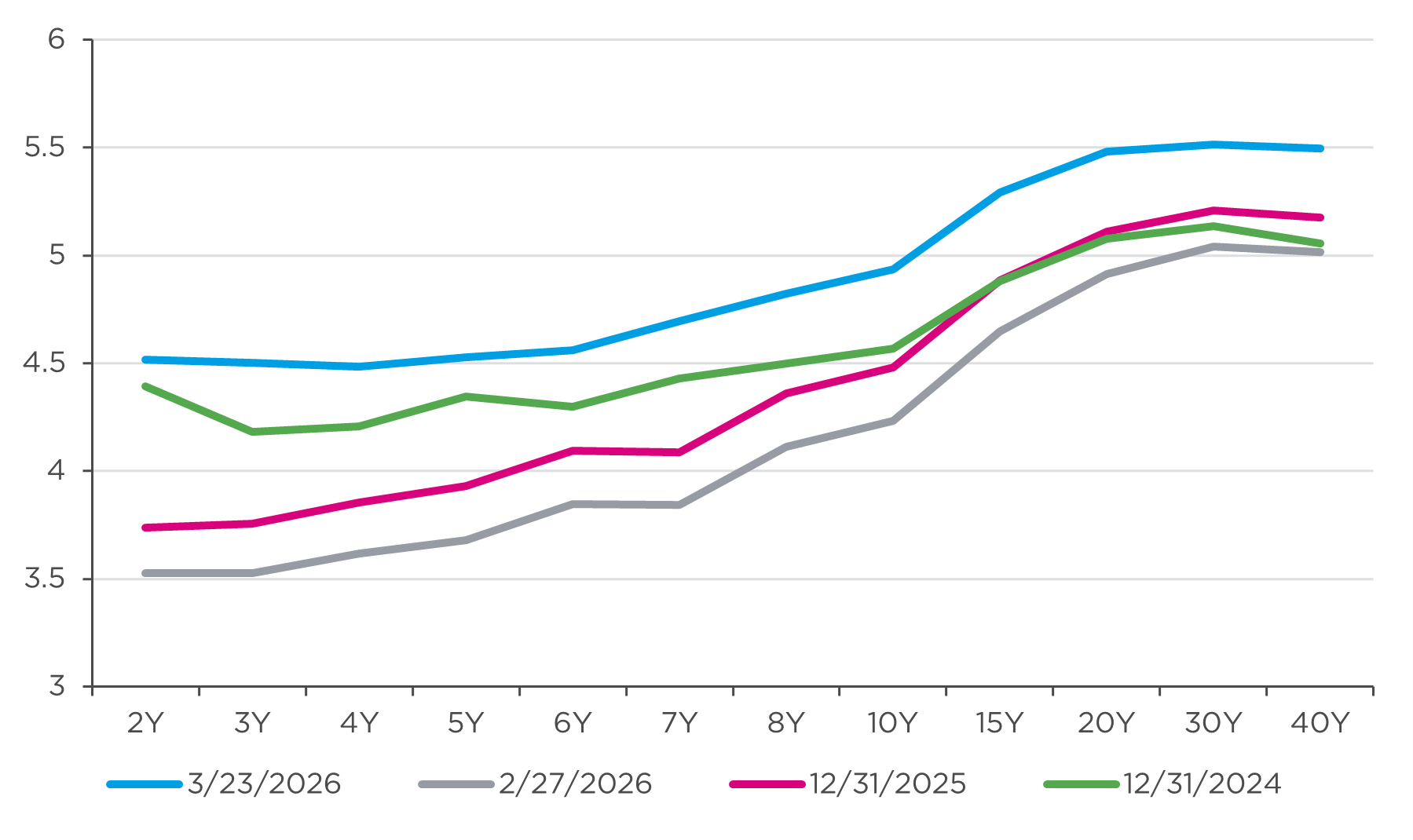

The market for short-dated UK government bonds (‘gilts’) underwent a similar correction. The yield on two-year gilts saw its biggest daily increase since the ‘mini-budget’ crisis of September 2022. As a result, the government’s borrowing cost increased, which will affect its budget.

Figure 3. Short-dated gilt yields were falling until February 2026, but they rose sharply in March

Source: Bloomberg

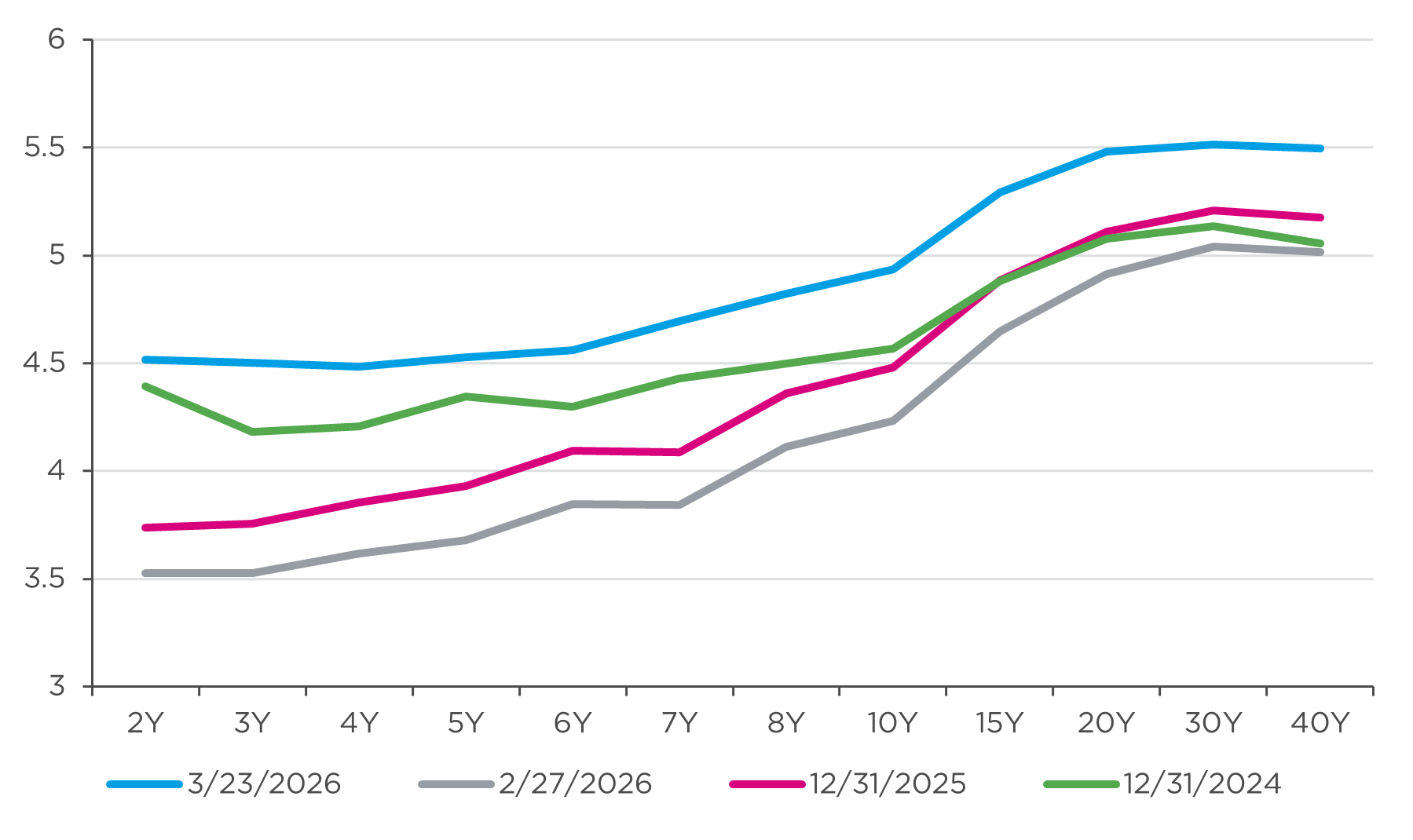

Figure 4. Longer-dated gilt yields have risen as well

Source: Bloomberg

What comes next?

Nobody can predict the course of this war, or what it will take to achieve peace. But the risk of escalation is significant, as illustrated by President Trump’s threat to ‘massively blow up’ the South Pars gas field. That course of action could disrupt Qatari supply even without Iranian retaliation.

Equally, de‑escalation remains possible, should the US or Israel declare that their strategic objectives, however opaque until now, have been achieved. It is clear, however, that higher energy prices and higher mortgage rates will feed through into the economy. These will further restrain an already weak trajectory for UK growth.

Here at CCLA, our interpretation is that the MPC is signalling its intent to maintain the current policy settings in the near term. The BoE’s Governor, Andrew Bailey, has reiterated that in interviews after the Bank’s decision last Thursday.

Second‑round inflation effects of the current rise in energy prices, such as rising food prices that could feed into wage demands, would be the principal trigger for a rise in the BoE’s Bank Rate. It is unlikely that those effects would become evident until later this year. Only then could investors form a more definitive view on whether the next move in Bank Rate will be upwards or downwards.