As featured in Room 151

The war in the Middle East has triggered a rise in energy prices that affects different parts of the world in different ways. The US economy is substantially insulated from world prices: it produces nearly twice as much oil as Saudi Arabia, with a Strategic Petroleum Reserve and, possibly soon, access to Venezuelan oil.

Europe and the UK, by contrast, are net oil and gas importers, including substantial imports from Qatar. Asia’s dependence on Middle East oil has risen in recent decades. Upward pressure on Asian manufacturing prices could contribute to higher inflation in the rest of the world.

As we go to press this lunchtime, Monday 9 March, our hopes for a de-escalation of hostilities have not materialised. Instead, one Khamenei has been replaced by another, his son, as Iran’s Supreme Leader. As a result, the price of Brent Crude oil spiked around $118 per barrel this morning, although it has now returned to $105 per barrel—nearly $40 higher (!) than its February low. Prices for natural gas have surged as well, by more than 60% over the last week.

Higher inflation affects us all

At the start of February, the Bank of England (BoE) expected consumer price (CPI) inflation in the UK to return to 2% this spring. That now seems unlikely. Instead, many financial analysts fear that the latest energy price rises will feed into the broader economy. Broader price rises would not just affect utility bills and transport costs, but food prices and industrial production as well. If energy prices stay near their current levels, inflation might pick up again, to 3% or higher.

Higher inflation makes near-term interest rate cuts by the BoE less likely. At the end of February, investors expected the BoE to cut its Official Bank Rate from 3.75% now to 3.25% by the end of the year. They now, on average, expect the BoE not to cut interest rates at all this year. That, in turn, could dampen economic growth.

Looking further out, yields on two-year gilts (UK government bonds) have risen from 3.42% at the end of February to 4.10% today, and ten-year gilt yields from 4.41% to 4.75%. Rising gilt yields show that, beyond fears for higher inflation, investors worry about UK economic growth, about the government’s finances and about its debt burden. This creates an unwelcome déjà-vu for Chancellor Rachel Reeves, as we pointed out in late 2025 (How interest rates and GDP will guide the autumn budget).

Rising interest rates have consequences in treasury management

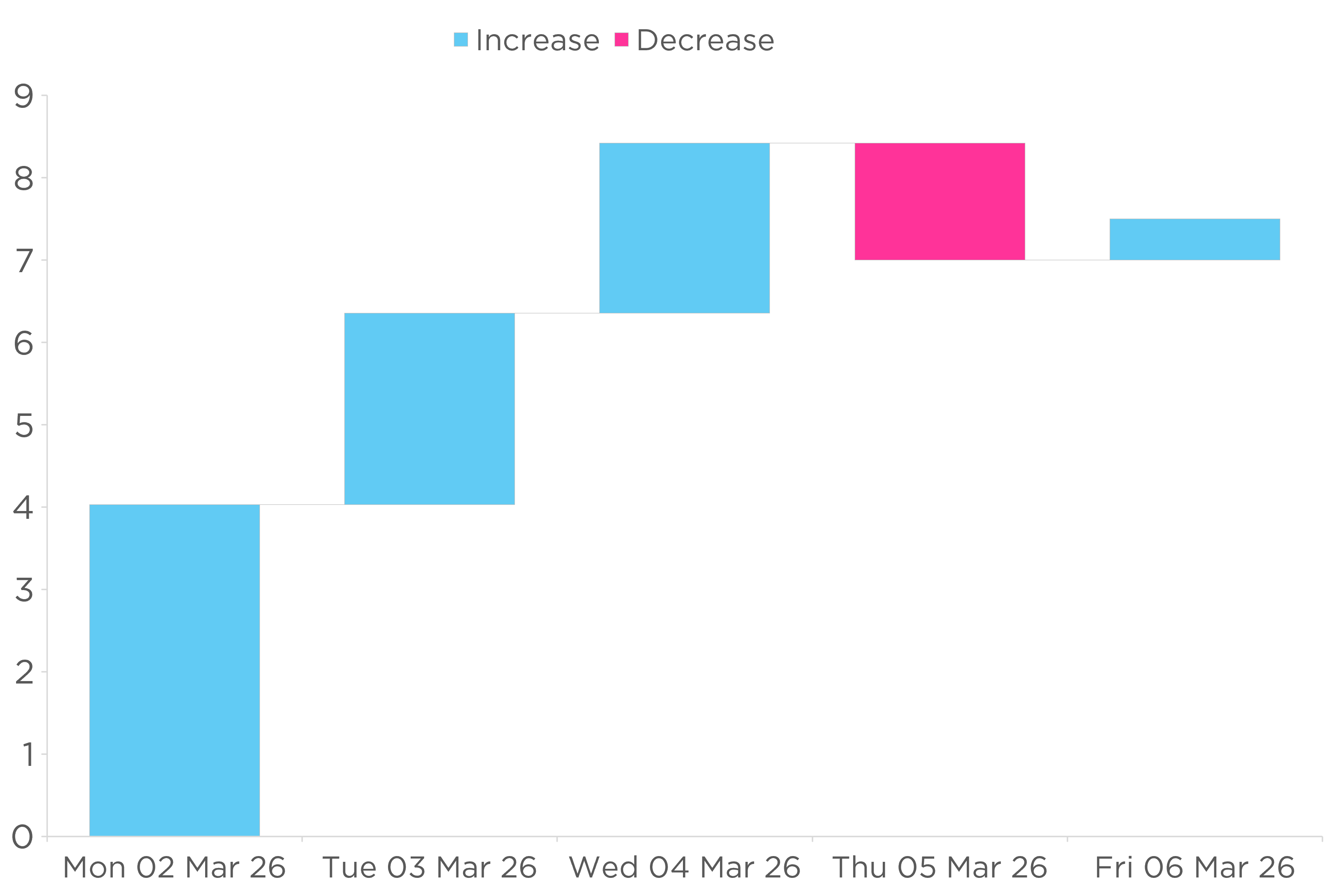

War and political turmoil typically lead investors to reduce risk and increase their holdings of liquid assets such as cash and money market funds. These last weeks have been no exception. In the first week of March, for example, investors funnelled more than £7 billion into so-called LVNAV (‘Low Volatility Net Asset Value’) funds. LVNAVs are a type of money market fund that aims to provide capital security and daily liquidity.

Figure 1: Sterling money-market funds registered over £7 billion of inflows in the first week of March.

Source: CCLA, Bloomberg

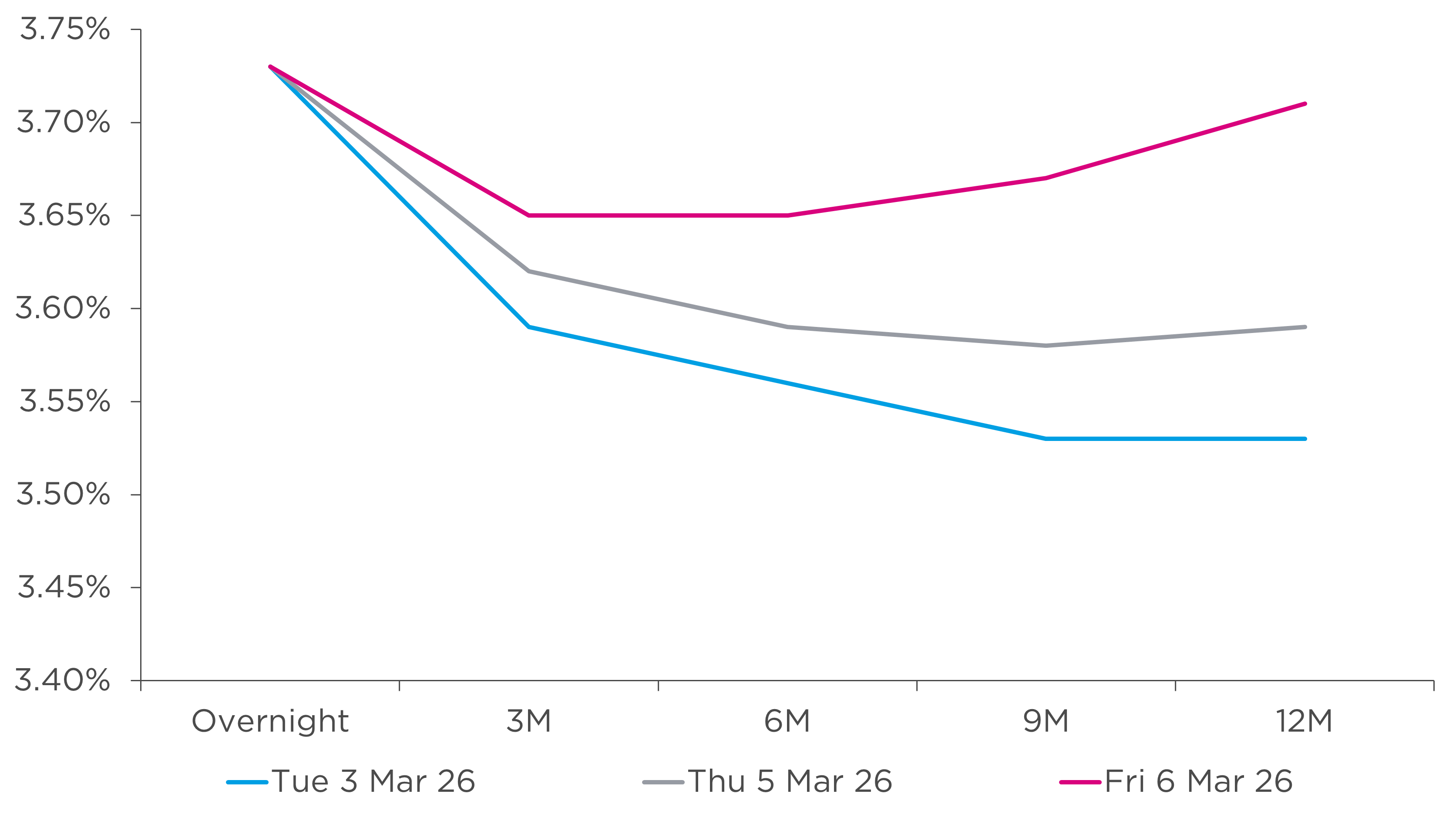

As figure 2 shows, market expectations of one-year sterling interest rates have increased by more than 0.40% in less than a week’s time. When money market rates rise, the interest rates that LVNAVs pay typically rise as well. We have, for example, in recent days added Certificate of Deposit positions that yield more than 4% p.a. By contrast, we have seen no moves by retail banks to increase the interest rates they offer on current or savings accounts.

Figure 2: In less than a week, one-year sterling interest rates have increased more than 0.40%.

Source: CCLA, Bloomberg

Conclusion

Given the fast-moving situation, please bear in mind that our current view is based on just over a week of conflict. But until our wish for peace becomes a reality, energy markets are likely to remain volatile and upward pressure on inflation may be here to stay. That, in turn, will put upward pressure on the Bank of England’s Official Bank Rate and on UK bond yields. The current geopolitical backdrop highlights the value to treasurers of having diversified, well-managed liquidity that can benefit from short-term rate rises while preserving capital.