15 October 2022

Much has been written in recent weeks on the ill-fated UK ‘fiscal event’ set out on 23 September and its impact on the value of sterling and the UK fixed interest markets. The pressure on some UK pension funds was so extreme that they reached breaking point with the Bank of England having to intervene in an attempt to restore orderly market conditions so that no pension fund defaulted.

This update does not give a timeline of the events since 23 September as it would have been out of date by the time of publishing. Instead, the article looks at how CCLA has managed the £3.5 billion of investments within its three Deposit Funds through this “once in a generation” market turbulence and how the funds will invest over the coming months.

Background

After 18 months with interest rates at historical rock bottom levels, even at times flirting with the prospect of moving negative, markets and then eventually the central bankers came to terms with the fact that the inflation outlook was no longer benign as the world moved out of the pandemic shutdowns. Initially we witnessed a slow but steady increase in money market rates as the prospect of rate increases moved into the forward-looking projections. In response we made a number of long dated investments to lock in on those enhanced rates which were on offer.

The Bank of England began tightening monetary policy in December 2021, when the Monetary Policy Committee (MPC), which sets policy to meet their 2% inflation target, voted by a majority of 8-1 to increase its Official Bank Rate by just 0.15 percentage points, to 0.25%.

Around that time, we were directed by perhaps the most hawkish member of the MPC, Michael Saunders, that:

it is likely that any rise in Bank Rate will be limited given that the neutral level of interest rates remains low. Provided we do not delay too long, it should be a case of easing off the accelerator rather than applying the brakes1.

This very slow, but steadily increasing projection for interest rates, continued to offer some attractive opportunities to make longer dated investments, however this picture changed in February 2022 as energy and commodity prices skyrocketed in response to Russia’s invasion of Ukraine.

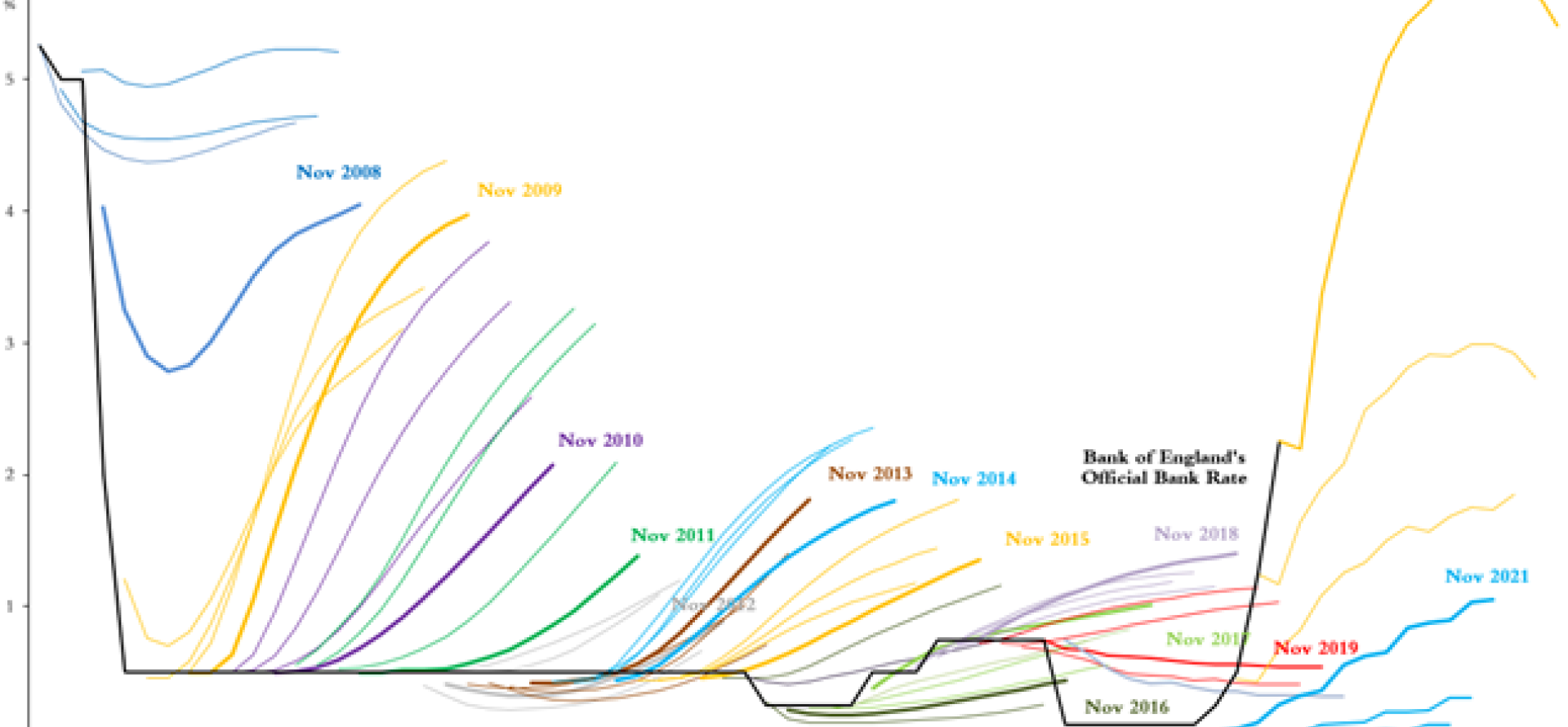

Since the invasion began, inflation expectations have consistently been revised upwards, we have seen hikes at every MPC meeting since and crucially expectations for future interest rates have continued to accelerate (see Chart 1). In February we took the decision to limit the longer investments made by our funds and bring our average durations down. We then hastened this approach as the economic conditions and inflationary environment over the year deteriorated.

Chart 1

Source: CCLA and Bloomberg as at 14 October 2022.

Our fund management approach since the ‘fiscal event’

The COIF Charities Deposit Fund and Public Sector Deposit Fund follow the FCA UK Money Market Fund Regulations (MMFR) and are classified as Low Volatility Net Asset Value (LVNAV) funds. Within this regulation, LVNAV funds have a regulatory limit of 20 basis points for the difference between the market value of its assets per pound and the constant value of £1. In constructing the MMFR, the politicians and regulators intention was to force fund managers to take less risk and increase the liquidity of the MMF products, they believed the new 20 basis point ‘collar’ would achieve this.

However, the inclusion of the ‘collar’ actually added a new Event Risk; when there is a sudden exorbitant movement in interest rates, it could lead to the Fund moving out of its ‘collar’, causing the value of a deposit/investment to become variable. This is a situation all Managers of LVNAV funds need to try and ultimately avoid, as Fitch Ratings have previously noted2, that a breach in the collar would be viewed as a ratings event and any change in either fund’s AAAmmf status would likely make the fund far less attractive to depositors/investors.

After the then Chancellor made his pro-growth strategy announcement we observed an unprecedented rapid repricing of interest rate expectations, at one point, rate increases were projected even before the November MPC meeting. We, as Fund Managers, were concerned that we were unable to predict where this repricing would stop and no real ceiling was evident. As we were unable to judge whether a three-month investment, for example, represented good value, our investment approach was to hold fire, we were reluctant to take on any significant duration risk until some stability and certainty returned.

In addition to our concerns surrounding investment values, these sudden changes in interest rate expectation presented sterling money market fund managers with an issue not experienced under the current regulatory regime. Despite the fact we had deliberately been lowering the weighted average maturity of the funds, as described above, the turbulent money market repricing meant the yields on our investments, made prior to the fiscal event, no longer reflected the new interest rate environment.

As there was such a high degree of uncertainty and in line with fund policies, CCLA made the decision that we would limit the maximum tenure of Fund investments to just one week in order to keep the funds comfortably within their ‘collar’. Shortly after the immediate uncertainty subsided, CCLA relaxed this restriction to allow for one-month investments. This approach has served the Funds well and the difference between the market value of its assets per pound and the constant value of £1 has receded markedly but it is still a little higher than typically one would expect.

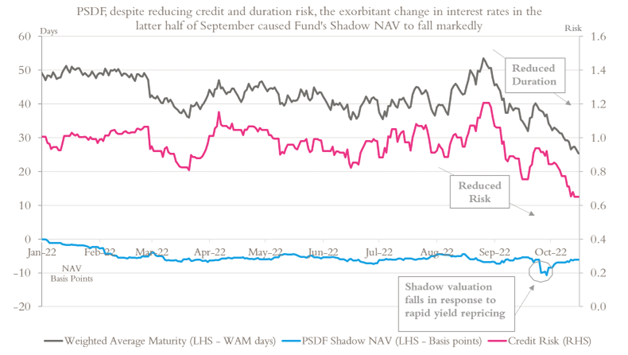

While these restrictions have meant the funds have not taken opportunities to trade at very attractive levels, sometimes in excess of 5.50% in the one-year tenures, CCLA’s approach has been consistent with our low-risk strategy of putting security and price stability always above yield. Chart 2 sets out how we have reduced both duration and risk within the PSDF over recent weeks, as well as the movement in the shadow NAV:

Chart 2

Source: CCLA as at 14 October 2022.

Over this heightened period of volatility, other money market funds with large institutional client bases have seen substantial flows both in and out as their clients have had to cover margin calls resulting from volatility in other investment markets. Many of these funds are the same as those which saw huge outflows at the start of the COVID pandemic. We are in the fortunate position that our funds benefit from a church, charity and local authority client base not usually susceptible to sudden cash flow requirements caused by market volatility. This is why our fund sizes have not seen any unusual movements; we look at our client base as a strength, as it means our funds are less likely to need to sell assets to raise cash in stressed markets.

The coming months

While there still is extreme uncertainty surrounding the future path for interest rates, the one certainty is that they will remain on an upward trajectory for some months to come. The next MPC decision is on 3 November and the Bank of England appears to be laying the groundwork for a bumper hike. Governor Bailey said on Saturday ‘We will not hesitate to raise interest rates to meet the inflation target. And, as things stand today, my best guess is that inflationary pressures will require a stronger response than we perhaps thought in August.’3

As the funds have been limiting longer dated investments for some time now, they are well structured to react quickly to any outsized increase in Bank Rate. Using PSDF as an example, at the time of writing, 72% of the fund will be reinvested in the next month with 87% of the fund maturing within the next 60 days. The fund yields are also being further enhanced by the maturity of a number of the lower yielding investments made in late 2021 and early 2022.

While we continue to witness large volatility in interest rate projections, our investment approach will remain focused on keeping the Fund’s duration lower than in recent years. However, we may look to make some investments into early January to ensure the Fund is strongly positioned for what looks like a difficult and complicated year end for markets.

While 2022 has been a year unlike any other when it comes to market volatility and shocks, I hope this update highlights how the continuation of our low-risk approach to fund management, always prioritising security and liquidity over yields has helped to protect fund valuations and keep the funds in a strong position as we approach the year end.