- For the last few weeks, all eyes have been on the Middle East. But in the months before that, artificial intelligence (Al) had been the dominant narrative, which it might become again when peace returns.

- Last year's prevailing narrative was that Al will boost the world economy. This year, by contrast, investors worry that Al is a threat to traditional businesses.

- This 'Al threat' narrative hasn't just affected software and tech shares. It is impacting industries ranging from insurance to banks, data and even catering.

- When others are fearful, we aim to keep level heads. A considered approach, based on fundamental analysis, can identify businesses that withstand Al disruption. Some of those businesses are now attractively valued.

What's behind the recent change in tone about Al?

The stock market started 2026 much like it ended 2025, dominated by the theme of Al. Only, this year, that narrative hasn't been about the growth that Al will generate. Instead, it's been about the supposed havoc that Al might wreak on long-established companies.

The software sector is at the forefront of this threat. Vibe coding, for example, is quickly becoming mainstream. This is the notion that, with the help of Al, anyone can write software code using everyday language and create applications in a fraction of the time that software engineers need. 'Vibe coding' has supported the notion that so-called 'Al agents' will replace traditional tools to write software, or at least lower the prices that software companies charge for them.

Other new launches this year, such as Al firm Anthropic's Claude Cowork, have turned Al from mere chatbots into enterprise-focused work agents that act as additional colleagues. This has changed the market's view of what's possible with Al, and further innovation is widely expected.

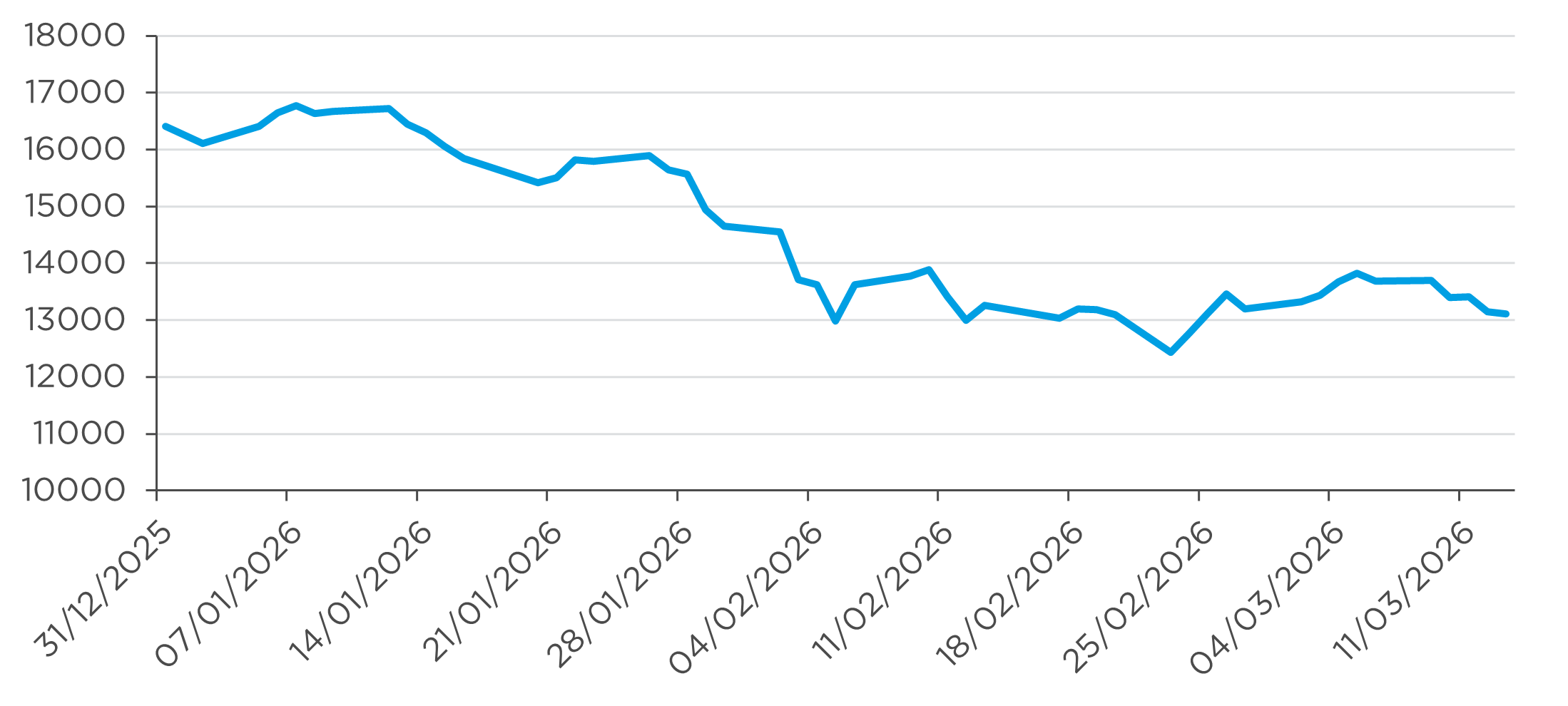

Figure 1. The S&P Software & Services stock market index has fallen by 20% since the start of 2026, mainly due to fears over Al disruption.

Source: S&P, as of 16 March 2026

Al disruption is more than a technology story

Fears about Al disruption aren't only impacting the software sector. They have soured most stock market segments, ranging from insurance to catering, with many investors taking a 'guilty until proven innocent' approach.

In mid-February, for example, OpenAI approved several consumer insurance apps to run on its ChatGPT platform. As a result, the share prices of several corporate insurance brokers fell steeply. But the ChatGPT-approved apps in question focus on personal insurance such as car and home policies. They don't operate in the complex commercial markets for, e.g., directors' liability and professional indemnity policies, where the brokers whose share prices fell are active.

Other examples of the Al disruption theme: share prices of wealth management businesses have been weak, as investors assess if Al might disrupt the market for financial advice. Even banks, until recently touted as Al winners because of possible cost savings, now face investors' fears that competition for depositors will rise in an Al world.

To cap it all off, New York-based Citrini Research published a dystopian outlook in February ('The 2028 Global Intelligence Crisis'). In it, Citrini forecasts that Al will lead to mass unemployment, collapsing consumer demand and a stock market crash.

In response to Citrini's research, the share prices of software firms such as Datadog and CrowdStrike fell more than 9% in a single day. Again, the fall-out from this report wasn't limited to IT: share prices of market infrastructure names such as American Express or Mastercard, for example, also fell on the suggestion that Al could lead consumers to bypass them.

Some investors use remedies that are worse than the disease itself

Investors' search for safe havens to protect against Al disruption has led to uncommon stock market situations. In February, for example, share prices in defensive sectors, such as consumer staples firm Walmart, rallied at the same time as those in cyclical sectors, such as machinery firm Caterpillar.

That synchronicity is exceptional and results from a safe-haven strategy known as the HALO trade, an acronym that stands for 'Hard Assets, Low Obsolescence', in which investors seek out physical moats that Al cannot easily disrupt.

The HALO trade has, however, seen some investors pile into capital-intensive businesses without remembering that those, historically, have struggled to sustain high returns over the long run. Share prices for metals and mining companies, for example, are down more than 20% in the month to date. Shares of industrial firms and consumer staples businesses are down more than 10%.

Private-market narratives versus fundamental stock market analysis

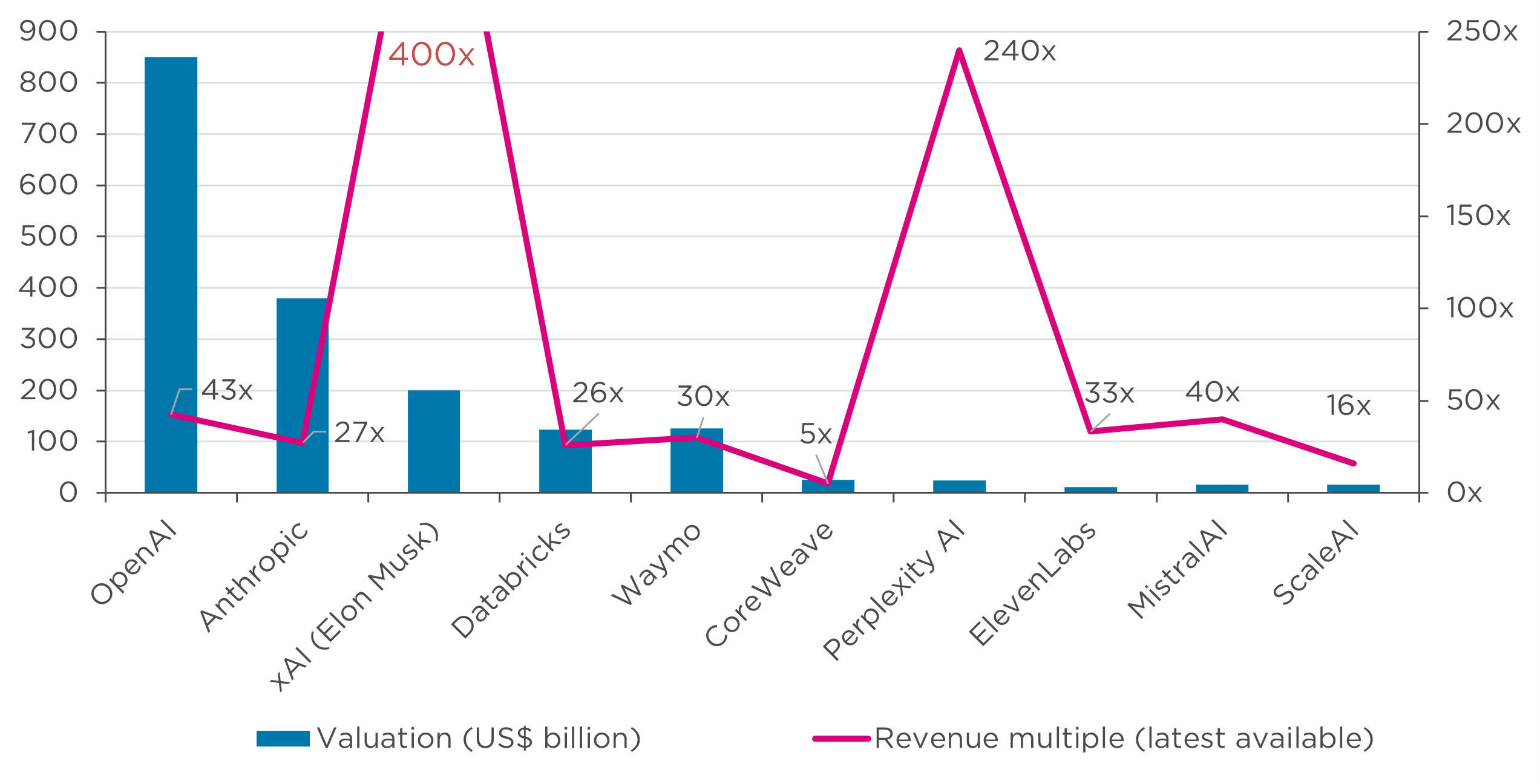

It is estimated1 that there were over 70,000 Al start-up companies, which absorbed c. $259 billion in venture capital funding last year. Most of these Al companies aren't publicly listed on any stock market. Instead, their often high valuations as private companies are mostly based on revenue multiples, and reflect their investors' high aspirations to upset entire industries. By contrast, most publicly listed tech companies trade, more conservatively, on earnings multiples and profit margins.

For example, Open Al, the American company that developed ChatGPT, recently raised $110bn, the largest fundraising in history, valuing the business at $850 billion. The company generated just $13bn in revenue last year, but it is targeting revenues of $280bn by 2030, as much as 50-year old Microsoft in 2025. Likewise, Anthropic, the owner of Al tool Claude, recently raised $30bn, valuing the company at $380bn.2

Figure 2. Private Al companies trade at large valuation premiums. Will they be able to justify those premiums when they become publicly listed companies?

Source: Al Funding Tracker, TechCrunch

Both Open Al and Anthropic may want to list their shares on the stock market as soon as later this year. It remains to be seen if their rumoured valuations will prove realistic, and if their products continue to be revolutionary. These companies' existing investors, however, have a vested interest in propagating the current Al narrative. And because of their disruption narrative about these private companies, many publicly listed companies' shares are trading on fear, rather than rational industry analysis.

We, by contrast, prefer to take a more considered approach, grounded in fundamental analysis of companies and industries. We have, for some time, been considering the risks and opportunities that Al technology brings to different industries, which led to several changes in our portfolios in 2025.

Our analysis does not point to impending Al Armageddon

Recent developments in Al are significant and should not be under-estimated, least of all in the software industry. But it is unwarranted to assume blanket weakness in companies across many industries, especially when these companies continue to report strong and improving earnings for the foreseeable future.

Disruption risk is higher and more evident in some industry segments. Consumer-facing software platforms such as Adobe, for example, are having a tough time competing against rapidly growing new, Al-based entrants such as Figma or Canva. In marketing, Al is changing the way campaigns are designed and run. And in the call centre industry, Al is increasingly handling high volumes of interactions, replacing human agents at a fraction of their cost.

However, many software companies have business model characteristics that, in our analysis, offer significant protection. For example:

- Some software tools are deeply embedded within organisations' workflows, and serve their critical operations, such as those provided by enterprise software firms SAP or ServiceNow. Any Al tool would find this kind of software hard to displace, as the barriers to switching are high, as is the potential cost of a failed switch.

- Proprietary data sets, not accessible to new Al entrants, are a valuable competitive advantage as well. Take, for example, the decades of price data owned by London Stock Exchange Group (LSEG). Microsoft, OpenAI, Anthropic and other Al firms have all come to partner with LSEG . LSEG will continue to own the stock market data these companies buy licenses to use. But distribution on Al platforms makes it possible for LSEG to significantly increase the usage fees it earns and expand its customer base.

Deep domain expertise and the trust built up with clients are important differentiators, as in the case of information and analytics firm RELX. Al is helping RELX increase its addressable market.

In RELX's legal division, revenue growth has accelerated from 6% in 2023 to 9% in 2025 with tools such as Protege, an agentic legal assistant.3

- Finally, incumbent firms have opportunities to embrace Al and innovate their offering, just like new Al entrants do. In addition, many incumbents are improving their engineering productivity and their profitability, again driven by Al tools. That is already the case with the companies mentioned above, LSEG and RELX.

Investors deserve a balanced view

Some investors focus on the next threat at hand when setting their investment strategies. The ongoing war in the Middle East has grave financial and human consequences, but it is not the sole focus of our attention.

Al remains a rapidly evolving technology that is likely to have profound implications for consumers, businesses and economies. But Al is at an early stage, and it is difficult to define who will be the winners and the losers.

Until then, Al may alternately boost and depress stock markets, much like the emergent Internet did in the late 1990s. Even after that 1990s dotcom boom (and bust), however, online and off-line successes continued to co-exist. Amazon thrives in retail, but so does its predecessor Walmart. ASOS has done well in fashion, but Inditex (Zara) remains a flourishing business. Airbnb is successful, but Marriott hotels are also finding new ways to grow.

It is all too easy to get caught up in the narrative that Al is a threat to every other industry, especially when that narrative serves the vested interests of a few venture capitalists. Instead, we are wary not to fall prey to either greed or fear, and we take a more considered approach.

Such a considered approach includes focusing on companies' fundamentals, while carefully monitoring downside risk. It also means considering the very real possibility that incumbent software, data and other companies may grow faster and more profitably with the help of Al.

1 Sources: HubSpot, OECD

2 Sources: Crunchbase, Fortune, Reuters